Understanding Earned Value Made Easy!

From WBS to Performance Measurement Baseline

Earned Value (EV) has grown in popularity over the years. With 76% of IT projects failing (Crawford, 2002, 19), project management and control systems must be utilized to ensure project success. Earned value is a valuable tool that often is not utilized because it is misunderstood. The purpose of this article is to provide a simplified approach to understanding earned value. Earned value is an early indicator and forecaster of project progress. Earned value shows a “three dimensional” view of project progress. Find out how earned value links to the work breakdown structure, the schedule, and the budget. If you read on, you will see the potential for implementing an earned value methodology on your projects, starting now!

To fully understand earned value you must understand how the performance measurement baseline links to the WBS, the schedule, and the budget. If earned value is to be used it must first be understood. Often the confusion, and misunderstanding of how earned value management systems are created, results in the avoidance of this powerful project management reporting tool

Project control is often a primary focus for the project manager. What we strive to control is the project plan. The result of the project plan is a tangible outcome that can be quantified and measured. The triple constraint of scope, cost, and time must be negotiated to ensure a successful project outcome. At the foundation of the triple constraint is project scope. Often this is the most neglected aspect of the triple constraint. Management is notorious for demanding reports on budget and schedule status but not scope. Think of the last time a request was made for how the project scope was doing on your project. Project scope is maybe the most difficult aspect of the triple constraint to quantify and measure. What we do have at the disposal of the project manager is the Work Breakdown Structure (WBS). Activity based estimating allows the work duration and cost to be assigned at a detailed level of project execution.

Once the WBS is developed a schedule can be determined. Then cost and duration can be assigned. This allows for the cumulative cost curve to be developed. This rate at which the spending is planned to occur is what EV can be measured against. The cumulative cost curve can identify the value at any point in time of the work that is planned to be done – this is called the Planned Value (PV). We can measure and ascertain the percentage of the work done. The cost of the planned work that was actually spent can also be determined. With this information you are armed with a powerful tool to manage the project – EV.

Earned Value

Earned Value (EV) has grown in popularity over the last number of years, possibly due to data like Phillips (2002) which quotes the Standish Group as reporting on IT projects:

- 31% of projects are canceled before completion

- 88% are past deadline, over budget or both

- For every 100 starts, there are 94 restarts

- Average cost overrun is 189%

- Average time overrun is 222%

Defining the Scope

The WBS

To fully understand EV we must understand how the values are developed. First start with the Work Breakdown Structure (WBS). By definition the WBS is “a deliverable-oriented grouping of project elements that organize and defines the total scope of the project”. (PMBOK© Third Edition, 2004). This in its most basic explanation is a list of all the tasks or activities that must be accomplished to deliver the project. A properly developed WBS is dissected into parts that represent a unit of work. Through the years the infamous “80 hour” rule has been handed down from generation to generation of project managers. I have even heard of project managers that keep the unit of work down to 40 hours. Why is this? When you try to assess how you’re doing – looking at 40 or 80 hours is much easier to assess than 2 months of work. If you can make better assessments of activity progress you will increase the accuracy and validity of your reporting.

How far do you break down a task? I always say, “To the level that makes sense”. For customer reporting you would go to a different level of detail than you would for management reporting and yet again to a different level of detail for the employee who will do the work. The objective should be to break the work down into parts that can be measured and identified that they are completed while not exceeding 80 hours. Using common sense is best when determining this. Keep in mind that the WBS is a tool to help manage your project; it is not a tool to micro manage.

The lowest level that you dissect the WBS to is the “work package”. By definition the work package is “a deliverable at the lowest level of each branch of the WBS”. (PMBOK© Third Edition, 2004). These are the activities that duration and costs will be assigned to. Once again, remember not to exceed the 80 hour rule.

Now that a WBS has been developed we can estimate the time and cost for each activity. Let’s reassess what we have so far. We have a WBS that consists of several levels; the project, its deliverables, tasks, and activities.

Other Scope Defining Products

What else do you have? You can look to contracts, statements of work, requirements, and other organizational representatives that may have been involved in development of the project plans (or whatever you may call them) available at this point. You also have Subject Matter Experts (SMEs) and those that will do the work. At the very least I am hoping that they are included! They have valuable inputs and need to be factored into the estimating process. You also may have access to project records of similar projects. If you do not, start archiving project records. This will help you to develop best practices as you develop your organization’s project management maturity.

Estimating Duration

Time estimating is your next step in this process. We have a very rough estimate that the work package can be done in less than 80 hours. Possibly there is a need for a more detailed WBS for the technical teams that will work on specific parts of the project. As you analyze each work package or activity, consider the time it would take under normal conditions, optimal conditions, and worst case conditions. Estimates should be realistic and there are many tools that can be used to minimize the risk that a project might run late.

Task Sequencing

When looking at tasks in a project, a strategic planning session should occur to determine task sequence. Think of this as a game of chess. Analyze the best sequence for the project tasks. Establish dependencies, mandatory and discretionary. This is a powerful use of the infamous post-it note. They can be placed and moved at will. Once all the tasks have been laid out they can be placed into a scheduling software tool of choice. Remember the software is a tool to help you with reporting; it is not project management, any more than using a word processor makes someone an author. Understanding the skills and tools required to manage projects is what makes you a project manager.

Estimating Costs

While estimating task duration, all resources should be considered, then all direct and (don’t forget) indirect cost can be computed. Remember the factoring of project duration when considering costs. Considerations regarding resource use for the time period of the task occurrence should be factored. Possibly the desired resource is not available. This will assist you in determining a reasonable and acceptable budget that you can manage your projects to. Costs can be calculated by industry inputs, subject matter experts, and cost modeling techniques. The goal is to develop a detailed budget at the work package level. Then you aggregate the costs to develop a total budget.

Cumulative Cost Curve

Now that you have a schedule and a budget, you can determine the rate of spending. This is a time distributed budget that becomes “the cumulative cost curve”. This spending curve is developed based on the planned schedule. The schedule indicates when the tasks occur and the tasks have a cost associated to them. This determines the rate at which spending occurs. Now is when the 80 hour rule will become important. With the tasks being dissected to less than 80 hours the validity of measuring the task to determine project progress is enhanced.

Earned Value Basics

Key Earned Value measures are:

- Budget at Completion (BAC)

- Earned Value (EV)

- Planned Value (PV)

- Actual Costs (AC)

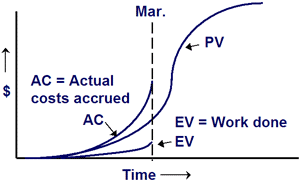

Figure 1

Budget at completion (BAC) and planned value (PV)

The cumulative cost curve can be used to develop the EV measures. The entire project value is the budget at completion (BAC). Specific points along the curve are called planned value (PV). When you decide the appropriate point to measure your project progress (this could be weekly, monthly, quarterly, or any divisible factor) you can look at your cumulative cost curve and determine what work packages should be done to that point in time and how much it should have cost.

Earned Value (EV)

When monitoring project progress the schedule can be utilized to determine what work has been done. If 70 percent of the scheduled work is completed (now aren’t you glad tasks are broken down to less than 80 hours?) the value for that work is 70 percent of the planned cost (PV) given for that portion of the work. Here is an example; through one month we had tasks totaling $100,000, this would be the PV. When we measured the work completed we determine that only 70 percent is done. This results in an EV of $70,000.

Actual Costs (AC)

Next we can determine the money spent to complete the work accomplished. This is referred to as actual costs (AC). Based on the previous example we might assume that the work accomplished is $70,000, but after all check is cleared we might have spent $85,000. Thus our actual cost for the $70,000 worth of work was $85,000.

EV Calculations

What does this all mean? You have a tool that provides a three dimensional view of the project. Typical project variance has been determined by looking at the difference between the planned and the actuals. Earned value lets you look at the planned values (PV), actual expenditures (AC), and the actual work completed (EV).

Schedule Variance (SV) and Schedule Performance Index (SPI)

The previous example showed us that we have a SV of negative $30,000. This is calculated by subtracting the PV of $100,000 from the EV of $70,000. This identifies that we did not do all of the work we said that we would ($100,000). We are behind the planned schedule. We can also determine a rate of work performed efficiency (SPI) by dividing EV by the PV. This results in a schedule performance index of 70.

Cost Variance (CV) and Cost Performance Index (CPI)

Also the previous example showed us that we have a CV of negative $15,000. This is calculated by subtracting the AC of $85,000 from the EV of $70,000. This identifies that the work accomplished did not cost what we estimated the work to cost. We have gone $15,000 over budget. We can also determine a rate of efficiency of spending (CPI) by dividing EV by the AC. This results in a cost performance index of .82.

Variance Ranges

Knowing the acceptable variance is a must for effective project management. What if the acceptable variance is 25%? We can determine that our budget estimating is acceptable by a CPI of .82. In regards to SPI we also can see that our schedule variance is unacceptable by a SPI of .70. We had better estimates for the cost of work than we did for the time to do the work. This is what we need to manage to. We can now better control our projects.

Predictive Measures

We can also predict where our project cost will end up. There are several Estimates at Completion (EAC) formulas. These formulas can be used to determine the upper estimates and the lower estimates. One of the formulas is dividing the BAC by the CPI so we can get a mid estimate. If our BAC for this project is at $1.5M, we can assume that with a cost performance index at .82, we will have an EAC of $1,829,268. If we subtract this value from the BAC we can determine the Variance at Completion (VAC) as -$95,744. Remember what I said about acceptable variance? If we have an acceptable variance of 25%, we would be within tolerance ranges. Twenty-five per cent variance on $1.5M equals $1,875,000, thus the EAC of $1,829,268 is acceptable.

Summary

What does this all mean? We have a tool, EV, which allows us to identify how much we should spend based on how much work we said we would do. But as all plans go, these are subject to change. We must determine acceptable ranges of variation when we first plan our project. How does an organization determine what an acceptable variance range is? First determine the level of difficulty for the project. Second determine the level of experience of those working on the project. Last determine how the organization assesses variance. I have seen organizations set variance levels as; +/- 10%, +/- 25%, +/- 50%, +10/-5%, +25%, -10%, and +75/-25. The different ranges should be articulated in the beginning and should be based upon the level of confidence that you can assign to your estimating efforts.

What have we learned? Earned Value is a control and monitoring system used to assess project performance. You can measure schedule progress, task progress, and cost progress. EV can be used to predict project performance and determine where the project will end up. Corrective actions can be taken to possibly put the project back on track or to stay within acceptable tolerance. We have identified that the values we use in EV are based on the WBS, schedule, estimates, and cumulative costs. Connecting these aspects will make EV an easy and valuable tool.

Go ahead give it a try!

References

Crawford, J.K. (2002). The strategic project office. New York, N.Y.: Marcel Dekker, Inc.

Phillips, J. (2002). IT project management: On track from start to finish. Berkeley, CA: McGraw-Hill/Osborne

A Guide to the Project Management Body of Knowledge, third edition, (2004). Newtown Square, PA. Project Management Institute.

Wayne Brantley, MS Ed, PMP, CRP, CPLP is the Senior Director of Professional Education for the University Alliance (www.universityalliance.com). Wayne has taught and consulted project management, quality management, leadership, curriculum development, Internet course development, and return on investment around the world to Fortune 500 companies. He is a certified Project Management Professional (PMP) by the Project Management Institute, a Certified Professional in Learning and Performance (CPLP) by the American Society of Training and Development, and a Certified Return on Investment Professional (CRP) by the ROI Institute. Wayne is currently an adjunct faculty member at Villanova University.

Peruvian Cocaine

… [Trackback]

[…] There you can find 61293 more Information to that Topic: projecttimes.com/articles/understanding-earned-value-made-easy/ […]

modesta

… [Trackback]

[…] Find More Info here to that Topic: projecttimes.com/articles/understanding-earned-value-made-easy/ […]

ชั้นวางสินค้าอุตสาหกรรม

… [Trackback]

[…] Find More Information here to that Topic: projecttimes.com/articles/understanding-earned-value-made-easy/ […]